Is the EU's single market leading to convergence or divergence?

The single market's 'agglomeration effects' – the tendency of wealthier areas to attract capital and skills – seem as strong as the 'catch-up effects' of poorer members importing capital and expertise.

Open markets are the best way of generating wealth and opportunities, of challenging vested interests and of expanding people’s freedom. But they also tend to concentrate wealth geographically, as a cursory look at the geography of any major market economy shows: people and firms often concentrate in particular regions or cities, because firms benefit from being near other firms in the same industry, where there are existing pools of skilled labour. Economic activity is concentrated within member-states of the EU, but what about at the level of the EU as a whole? The so-called ‘agglomeration effects’ of the single market – the tendency of capital and skills to concentrate in wealthier areas – seem as powerful as the ‘catch-up effects’ as poorer member-states import capital and management expertise from wealthier ones. To prevent persistent differences in living standards from undermining support for the single market, the EU might have to increase transfers between its wealthier and poorer member-states.

The EU’s single market may not be as integrated as the US one, but the degree of integration is nonetheless impressive. Many services markets are still predominantly local, but the degree of integration in goods markets and capital markets is very high. The latter is crucial: capital is free to move to where investors think it can be most efficiently used. In theory this should allow rapid income convergence as poorer countries import capital, innovations and management expertise from wealthier countries, and access bigger export markets. Countries and regions can then specialise, raising productivity and living standards.

But are these benefits of the single market enough to offset the agglomeration effects? Agglomeration economies or external economies of scale refer to the benefits firms accrue from producing in the same area as other firms in the same industry. For example, if a region specialises in the production of cars, it develops supply-chains, trains skilled workers, and builds infrastructure suited to that industry, attracting more firms in that sector. The integration of EU economies has given an impetus to agglomeration effects by opening up new markets for already competitive industries. A classic example is the German car industry, which has used its dominant position in the German market – the biggest in Europe – to carve out a dominant position in the single market as a whole.

The EU’s single market comprises three distinct elements: common institutions to create common standards; a common legal order; and transfers to weaker regions in the form of regional funds. These regional funds are supposed to help poorer member-states to adjust to the cost of market integration and are essentially a quid pro quo for opening up their markets to richer, more productive economies. Another part of the quid pro quo is labour mobility. Workers from poorer member-states are free to move to wealthier ones, boosting their living standards in the process, but potentially increasing agglomeration effects.

Workers moving from poorer to wealthier #EU members potentially increasing agglomeration effects

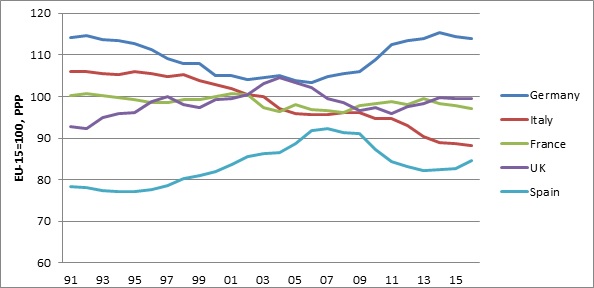

Are the forces of convergence or divergence gaining the upper hand? Let us take a look at the big five EU-15 economies first: France, Germany, Italy, Spain and UK (see chart 1). Adjusted for price differences, Germany is actually no wealthier relative to EU-15 average than it was in 1991, notwithstanding its relatively strong performance in recent years. France is somewhat poorer than it was 25 years ago, and Italy dramatically poorer. The UK has become somewhat richer, but even now is still below the average, albeit only slightly. Spain managed rapid convergence in the run-up to the 2008 financial crisis, but has subsequently given up around half of those gains.

Chart 1: Per capita GDP relative to the EU-15 average

Source: European Commission

One of the striking trends since the introduction of the single market is the success of smaller, already wealthy, EU economies. The biggest winners have been Austria, the Netherlands, Denmark and Ireland, but Belgium, Finland and Sweden have also become richer relative to the EU-15 average (see chart 2). The single market has allowed these economies to become increasingly specialised without running the risk of losing access to their big neighbouring markets.

Chart 2: Per capita GDP relative to the EU-15 average

Source: European Commission

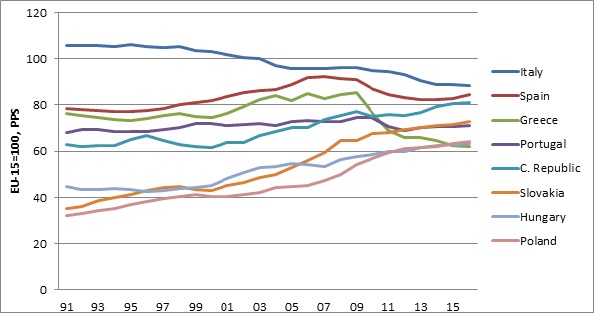

Easily the biggest losers – in addition to Italy – have been in Southern Europe. Greece is strikingly poorer than it was, and Portugal – the poorest EU-15 country until the onset of the Greek crisis – has barely converged at all with the EU-15 average. Indeed, they have been caught by the wealthiest post-communist Central and Eastern European members-states: the Czech Republic and Slovakia (see chart 3).

To a significant extent, the convergence between the poorest EU-15 countries and the richest of the countries that acceded to the EU in 2004 reflects the terrible performance of the poorest EU-15 economies, which has also dragged down the EU-15 average as a whole. For the last decade, per capita EU-15 incomes have been largely stagnant, although this masks big differences between countries. Had EU per capita incomes risen at a normal pace – 1.0-1.5 per cent per year – the central and eastern countries would have managed much less convergence. But this is not all of it: living standards in Central and Eastern Europe have also risen relatively strongly. They owe much of their income convergence to high levels of foreign direct investment, which has brought them into predominantly German supply chains, and driven rapid export growth.

Chart 3: Per capita GDP relative to the EU-15 average

Source: European Commission

The IMF’s medium-term forecasts give us as good an indication as any of whether these trends will continue. The IMF only forecasts per capita income at purchasing power parities exchange rates for the EU as a whole rather than just the EU-15. This amplifies the degree of convergence by including the poorer post-communist economies: their inclusion lowers the average. However, because the economies of these countries are relatively small, the difference between the EU-15 average and the EU is not huge, so using EU-28 data as opposed to EU-15 data still gives us a good idea of the likely trends. Convergence between the South and East will continue, Germany will remain considerably wealthier than the other big EU-15 economies, but some of the wealthy smaller EU-15 economies will face problems.

Convergence between the South & East will continue, but #Germany will remain considerably wealthier

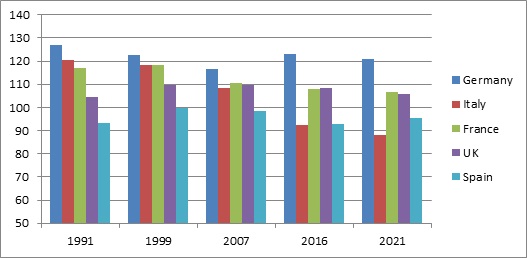

According to the IMF’s forecasts, there will not be any convergence between the big five EU-15 economies over the next five years (see chart 4). If anything, we are likely to see divergence within the group. Back in 1999, living standards (according to this measure) were broadly similar in France, Germany and Italy, somewhat lower in the UK and significantly lower in Spain. By 2021 this looks quite different. The astonishing decline in relative Italian well-being is expected to continue, as well France’s much more gradual decline. Spain and the UK are expected to hold their own, managing a bit of convergence with Germany. The overall picture is one of a sizeable, and persistent, gap in living standards between Germany and the other four economies.

Chart 4: GDP per capita, per cent EU average (in current PPP dollar prices)

Source: IMF, World Economic Outlook

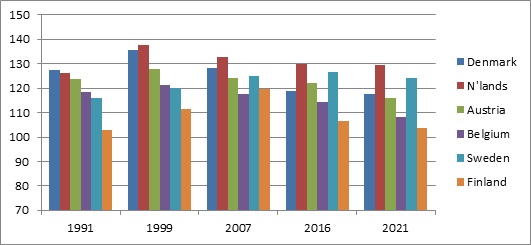

As for the small, wealthy EU-15 economies, while Denmark, the Netherlands and Sweden continue to perform well, Austria, Belgium and Finland fall back significantly (see chart 5). If these forecasts are right the smaller, trade-dependent economies may not turn out to be the big winners from the single market. One explanation could be that while the single market makes it easier for small economies to specialise, boosting economic growth, this specialisation then makes it harder for them to adjust to economic shocks because their economies are less diversified. The necessary adjustment could also be harder for members of the eurozone, because these economies have surrendered exchange rate flexibility and independent monetary policies.

Chart 5: GDP per capita, per cent EU average (current PPP dollar prices)

Source: IMF, World Economic Outlook

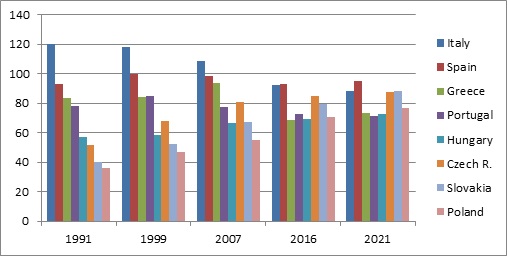

The story in the Central and Eastern European members of the Union is one of continued convergence (see chart 6). The Czech Republic and Slovakia close the gap in per capita incomes with Italy, and close in on Spain. However, perhaps the most striking trend is the degree of convergence in living standards between Italy and Poland, which by 2021 are forecast to have per capita incomes of 88 per cent and 77 per cent of the EU average respectively: as recently as 1999 the respective figures were 119 per cent and 43 per cent.

Chart 6: GDP per capita, per cent EU average (current PPP dollar prices)

Source: IMF, World Economic Outlook

The IMF’s forecasts, like all macroeconomic forecasts, need to be taken with a pinch of salt. Forecasting is notoriously difficult and sometimes political. For example, the IMF’s forecast of relatively rapid economic growth in Greece could reflect the IMF’s need to make the Greek bail-out numbers add up. However, few economists expect the Greek economy to rebound anywhere near as strongly as this. The forecast for the UK assumes that the British government succeeds in negotiating far-reaching access to the EU’s single market, which is unlikely. Indeed, there is probably a greater likelihood of negotiations between Britain and the EU breaking down, resulting in the UK leaving without any agreement in place. Under this scenario, the outlook for UK growth would be far worse than forecast by the IMF.

There are other question marks over the IMF forecasts. For example, will the post-communist Central and Eastern European economies really continue to grow strongly in the face of the backlash against liberal norms taking hold across much of the region? The erosion of the rule of law, mounting reluctance to open up their domestic economies to more competition and the increasingly unpredictable business environment could stunt growth.

Finally, the IMF’s forecasts assume that the eurozone avoids a further serious crisis. This is plausible: we could well still be relatively near the start of the economic cycle in the eurozone, implying that the bloc could experience several years of moderate growth between now and 2021. The Spanish recovery looks to have some legs, and France’s outlook appears to be brightening somewhat, while Italy’s remains poor. With the ECB having morphed into an activist central bank determined to raise inflation, and fiscal rules being interpreted more flexibly, it is possible that the eurozone will make it through to 2021 without a major upset.

But there are other possible scenarios: Marine Le Pen could win the French presidential election and hold a referendum on French membership of the euro. The next Italian general election could bring to power a coalition committed to a referendum on euro membership: the country’s main three opposition parties have all openly questioned continued Italian participation in the currency union. If either France or Italy abandoned the euro, economic growth across the eurozone, and indeed across the EU, would be much weaker than forecast by the IMF.

#EU might need to transfer more money between members if confidence in #SingleMarket not to erode

In conclusion, within the EU-15 there is little evidence of living standards converging as countries adopt best-practice from wealthier states and capital is deployed to where it can be used most productively. Indeed, there is some evidence of agglomeration effects centred on Germany, Benelux, the Nordics and Austria. The IMF expects a number of these economies – Austria, Belgium and Finland – to slow significantly over the next 5 years, but these are only forecasts; they may or may not turn out to be accurate. There is evidence of catch-up in the Central and Eastern European member-states, with the best performing overhauling the weakest EU-15 ones – Greece and Portugal – and on course to catch Italy within five years, at least at PPP exchange rates. But this must be seen against the unprecedentedly bad performance of the Greek, Italian and Portuguese economies.

The differences in per capita income across the EU are actually not much greater than across states in the US, so long as we exclude Bulgaria and Romania. But the US is a fully federal country with significant fiscal transfers through the tax, health and social security systems. The EU relies on labour mobility and structural funds to help bring about convergence. Labour mobility enables workers to boost their living standards by moving to wealthier states, but risks concentrating skilled workers and capital in the core, compounding fiscal pressures in poorer member-states. Structural funds are indispensable, but are small compared to the transfers within individual member-states or the US. There is little doubt the single market increases the size of the pie. The question is whether the lack of convergence in living standards is sustainable politically: can national governments continue to sell the single market to their voters if it appears some countries are benefitting more than others and if large differences in living standards persist? The EU might need to transfer more money between its member-states if popular confidence in the single market is not to erode. And it will certainly need to do so if the poorer member-states are to accept a deepening of the single market.

Simon Tilford is deputy director at the Centre for European Reform.

Add new comment