An unequal recovery would be politically explosive

When restrictions are eased, office workers will spend while poorer people, who have been more likely to get COVID-19, may struggle. Governments need to find ways to make the recovery fair.

The debate about austerity has already begun in Europe. Germany’s former finance minister, Wolfgang Schäuble, and the head of the German Chancellery, Helge Braun, recently suggested that national and European fiscal rules may need to be relaxed, causing a backlash among more hawkish fellow Christian Democrats. Rishi Sunak, the British Chancellor, is currently refusing to make permanent a £20-a-week uplift in unemployment payments, enacted during the first wave of the pandemic. Centre-right parties are still the biggest political forces in most European countries: in order to stop the populists and safeguard democracy and market capitalism, they must discover their inner social democrats. They – and governments led by the centre-left – should provide a pro-poor fiscal stimulus once vaccines allow social distancing to be relaxed, followed by tax and benefits reforms that shield poor people’s consumption from any attempt to reduce fiscal deficits. A rapid return to fiscal rectitude would lead to further stagnation, sending more voters towards the extremes.

Poorer people have been hit hardest by the pandemic. A rapid return to fiscal rectitude would prevent a recovery in living standards, sending more voters towards the extremes.

Politically, the combination of spending cuts, tax rises and weak income growth over the last decade has been highly destabilising. And the pandemic has hit poorer people much harder – measured not only in infections and deaths but also in lost incomes and jobs. When Europe’s finance ministers rushed through furlough programmes last spring, they did not cover 100 per cent of people’s wages, because they wanted to encourage people to work if they could. That was understandable, but it led more lower-wage workers to continue to work, often in jobs that could not be done from home, raising infection rates and deaths. Furthermore, companies that have been hardest hit by lockdowns in the hospitality, travel and tourism industries are most likely to get into difficulty, and jobs in these sectors tend to be low paid. Meanwhile, many office workers have continued to work and get paid largely as normal (albeit at home).

If the recovery is as unequal as the pandemic itself, the political consequences could be explosive. And because there is so much uncertainty about the future, governments need to err on the side of promoting a consumption-led recovery, even if that risks higher inflation: businesses will rehire workers and invest more rapidly if they can be confident about higher demand coming down the track.

There is a good case for optimism that the recovery from the pandemic might be the start of another ‘roaring twenties’. Well-paid office workers have built up savings during the pandemic, as lockdown and homeworking has given them fewer opportunities to spend. We will probably see a spending splurge once vaccines allow restrictions to be eased and economies to open up again. That hope has been reinforced by the sharp bounce-back in shopping and eating out observed in many European countries in the third quarter of 2020, when there wasn’t much COVID around.

However, European economies, particularly in Western Europe, were growing slowly going into the pandemic, and there is a risk that a mini-boom quickly peters out, leaving the continent with the same low-growth, inflation and interest rate economy that it had before. Richer people might also decide to hold onto some of their pandemic windfall rather than spend it, as they did, in part, with US stimulus cheques during the Great Recession. Richer people are more prone to saving any additional earnings than poorer people, who tend to consume all their disposable income. The UK looks especially vulnerable: private sector investment was flat between the referendum and the pandemic, and the growth of consumption was weaker than its peers. British exports will take a longer time to recover from COVID-19 than other countries thanks to the UK’s exit from the EU’s single market.

The other constraint on the recovery is the continuing uncertainty about the course of the pandemic, even after vaccinations in Europe have allowed something approaching normality to resume. As we have seen with the British, South African and Brazilian variants, COVID-19 is constantly mutating, and because developing countries will take much longer than the rich world to vaccinate, there is a risk that new mutations will arise in populations where prevalence of the disease continues to be high. Equally, COVID-19 might mutate in a more transmissible but less deadly direction, as other viruses have done, making it less dangerous over time. We do not yet know whether there will be further outbreaks after most Europeans have got their jabs, and the fear of further waves of infection might encourage more precautionary household saving and lower corporate investment.

With uncertainty so high, European countries need to promote a consumption-led recovery. That will convince investors that demand will be higher in the future, encouraging them to expand capacity now so that they can satisfy it. The EU’s recovery fund is largely focused on raising investment rather than consumption, and it will take some years for the money to have macroeconomic effects. Investment projects take time to plan, and the more that the money is rushed through, the more likely it will be spent on projects that do not do much to expand the supply side of the economy.

The recovery fund focuses mostly on raising investment and we won't see macroeconomic effects for some time. European governments need to promote a consumption-led recovery when lockdowns are lifted.

A short-term stimulus would be most effective if it put money in poorer people’s pockets. US-style tax rebates, but targeted at lower earners, would be the best policy, but may be too difficult to administer in time for the recovery. Failing that, the advantages of a VAT cut probably outweigh the disadvantages: it is simple to administer and would quickly boost spending across the economy and the hiring of furloughed and unemployed workers. Consumers would find they had more money in their pockets to spend; and they would bring forward the purchase of expensive durables, like cars. VAT cuts lead more quickly to higher spending than other forms of stimulus, and should result in a faster rise in output and decline in unemployment. There is a risk that firms won’t pass the VAT cut on to consumers in the form of lower prices, but that might improve their balance sheets and help them to rehire workers.

That said, VAT in most advanced economies is slightly progressive, meaning that poorer people pay less VAT than rich people, despite the fact that it is a ‘flat tax’ that is paid at the same rate irrespective of income. That is because poorer households spend more of their money on food, energy and housing, which have lower VAT rates or none at all. Therefore, cutting VAT will do less to put money into poorer consumers’ pockets than providing them with stimulus cheques (as Joe Biden is hoping to do in the US).

In 2022 or 2023, the surge of spending is likely to fall back again, resulting in the unsatisfactory growth rates we saw before the pandemic. The structural reasons for low growth have not gone away, such as ageing populations, lingering questions about societies’ commitment to the euro, high debt levels in some countries, a patchy single market that doesn’t generate strong enough incentives to invest and innovate, a culture that is at best grudging towards immigrants, and (for the UK) Brexit. All of those problems interact with inequality. During periods of faster growth, countries in the West tend to become more liberal and equal. They provide more civil rights, expand benefits, are more welcoming to immigrants and more co-operative with other countries. In periods of stagnation, they tend to be more authoritarian. And, as demonstrated by the Brexit process and the rise of autocrats in Central Europe, there is a risk that populism causes lower growth by encouraging economic nationalism or corruption. Making the European recovery faster and more equal will thus help to improve policy in other areas.

Once economies are operating at capacity, some fiscal consolidation will probably be needed, depending on the scale of the long-term damage wreaked by the pandemic. It is possible to reduce deficits while protecting poorer people’s incomes. The evidence is strong that raising redistribution does not reduce growth, as many conservatives have long argued, and may even increase it. Higher taxes may distort individuals’ decisions, reducing growth, by discouraging higher earners from working more. But that is offset by the fact that poorer people spend a higher proportion of their income than richer people.

What policies could governments pursue? It is tempting to fiddle with trying to reduce the bottom rates of income tax in an attempt to make them more sharply progressive. Alternatively, governments could provide larger social assistance payments for people on low incomes. The social assistance payments would be better targeted than the former, which provide tax cuts to richer people too, but both could lead to steep marginal tax rates for lower earners, which can discourage work. Raising tax rates at the upper end would be less damaging, but rich people are more able to avoid tax than middling and low earners. Tax rates on earned income are typically higher than they are on capital income or property: equalising income and capital tax rates would be a progressive move, because capital gains are more unequally distributed than earned income. Finance ministers could also end or reduce the tax deductibility of mortgage interest payments.

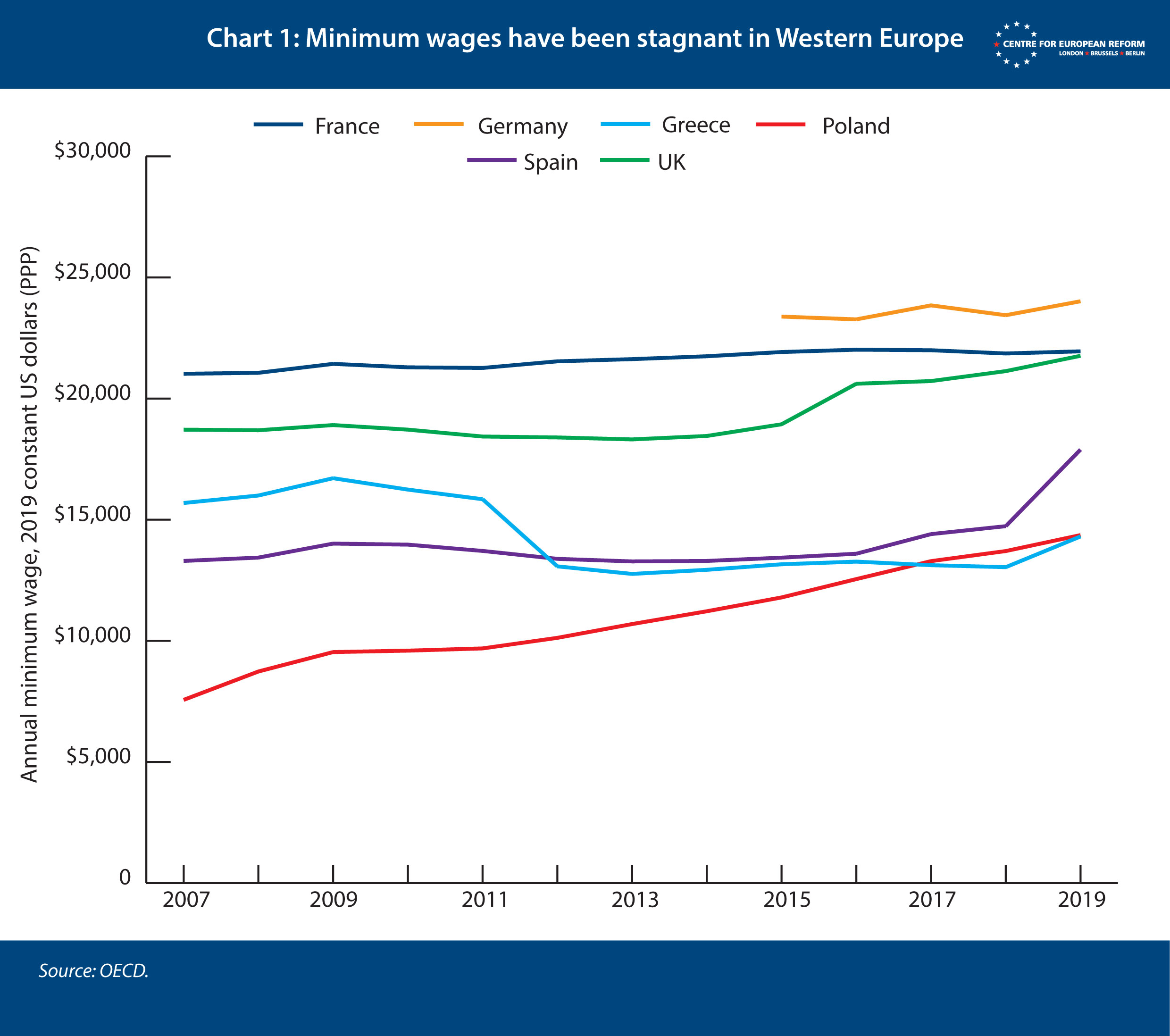

Raising minimum wages would also have an impact, especially after the recovery is complete. At some point higher minimum wages could result in higher unemployment. But in many European countries minimum wages have been stagnant in real terms over the last decade (although Spain and the UK have recently raised theirs; see Chart 1). What is more, the balance of evidence suggests that minimum wages up to around 60 per cent of the median wage have limited effects on employment and may raise productivity, either by forcing employers to improve productivity to make up for their higher wage bills, or by shifting workers to higher productivity companies. The average minimum wage in the EU is 50 per cent of the median, so there is further scope for slow and steady raises as the economy recovers.

But it is the provision of public services that may be most effective at reducing inequality. Universal childcare would allow more parents, often mothers, to avoid the pay penalty that having children imposes. More resources could be provided to schools with a deprived intake of pupils. An expansion of university places would make people more productive later in life, especially as employment in the services sector continues to grow. The share of adults aged between 25 and 34 who hold a degree is very low in Italy (28 per cent), and well below the EU average of 41 per cent in Germany, Sweden, Hungary and Czechia. As we have pointed out elsewhere, the long-running trend away from manufacturing and industry towards services has raised inequality across Europe by reducing the number of well-paying jobs available to people without higher education. It is also leading to a rise in regional inequality, with younger graduates increasingly concentrated in richer cities, pitting provinces against metropoles.

Targeted social assistance payments, minimum wage increases, and expanded childcare provision: these policies could all help European countries to make recoveries inclusive.

After the financial crisis, Europe’s social market economies frayed under austerity, and slow growth fed populism. Moderate politicians of left and right must not make the same mistake.

John Springford is deputy director of the Centre for European Reform.

Add new comment